The vaccine rollout and subsequent reduction in COVID-19 cases is giving parents and students hope for a return to normalcy this fall—and retailers are ready to bask in that enlightenment, new research from Deloitte reveals.

The overall outlook heading into the school year is bright, with 55 percent of K-12 parents and 46 percent of college parents more confident about the economy’s prospects (up from 17 percent and 14 percent respectively, in 2020), and household financial situations holding steady with 78 percent of K-12 parents and 75 percent of college parents in similar or better shape than last year.

As a result, parents are ready to spend, and the digital acceleration that occurred in the past year has created a new baseline for tech integration in the education system—altering not only the types of products needed for both virtual and in-person learners, but also how parents shop for them. Parents of college-age children are planning to spend more as well, with spending poised to reach record levels particularly among middle-income families and surpassing pre-pandemic levels.

As consumer sentiment improves and digital adoption increases, they will continue to impact not only how consumers approach back-to-school and back-to-college shopping, but how and what they purchase.

“As Americans anticipate a more traditional return to the back-to-school season, the good news is that parents are ready to spend more and earlier to ensure their children have what they need to be successful,” said Rod Sides, vice chairman at Deloitte, and U.S. retail, wholesale and distribution leader, in a news release. “This includes increased spending on technology for both K-12 and college students, demonstrating a shifting focus on how students learn as well as how parents are shopping for these necessities. We’ve entered a new era of schooling where traditional back-to-school supplies are fading in favor of tech, while consumers expect certain conveniences and competitive prices. Retailers that demonstrate their resiliency during this time will appeal to shoppers and be better positioned to capitalize on growing consumer sentiment.”

Back-to-school spending is bright for technology

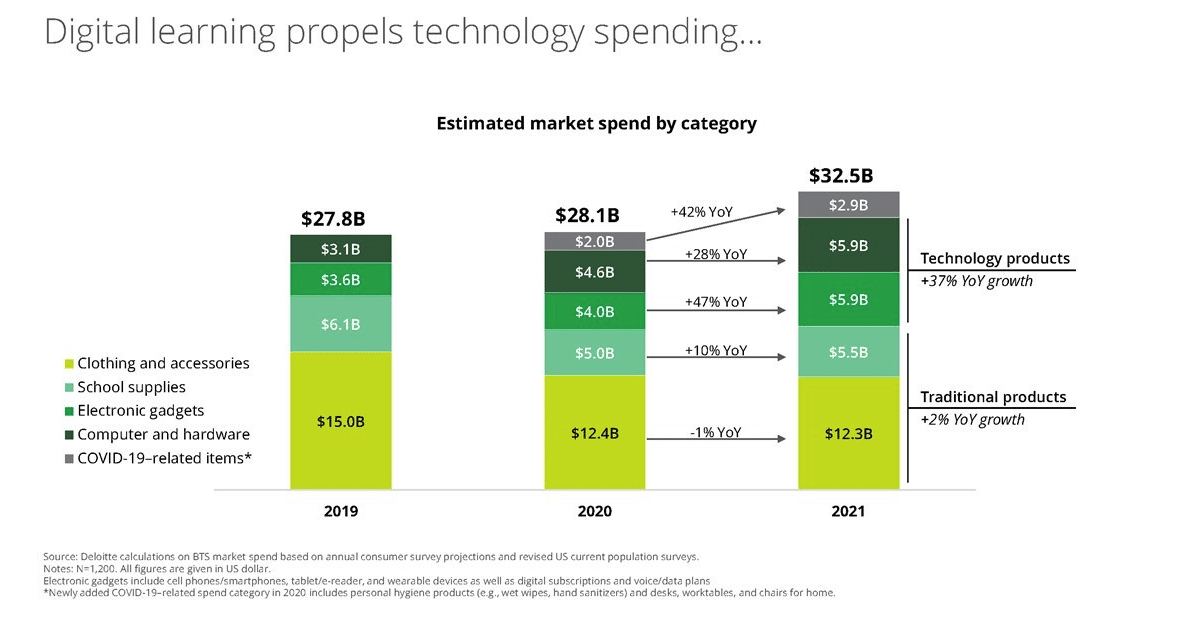

As many K-12 parents anticipate a more normal return to the classroom, back-to-school spending is expected to reach $32.5 billion, averaging $612 per student in grades K-12. This represents a 16 percent increase from 2020, which is the highest in recent years and greater than pre-pandemic levels.

- Overall spending will increase across categories with 40 percent of K-12 households planning to spend more on back-to-school items (up from 22 percent in 2020), including clothing, supplies, computers and electronics. The majority of these parents cite their children’s need for more items this year, as a reason for the increased spend.

- Spending on technology products (personal computers, smartphones, tablets, wearables, etc.) is set to increase 37 percent over 2020 to $11.8 billion, as parents adjust to the realities of a more digitally oriented education system. Wearable technology will see the biggest gain.

- Because their children are using more digital technologies in and out of the classroom, 44 percent of households plan to purchase fewer traditional back-to-school supplies.

- However, 58 percent will spend the same or more on online learning resources such as e-learning platform subscriptions, online courses, educational tool licenses and online tutors to supplement classroom learning.

“Like other industries, higher-education was forced into the digital realm during the pandemic, with colleges instituting hybrid formats seemingly overnight, originally planned to rollout in a matter of years,” said Stephen Rogers, executive director of Deloitte Insights Consumer Industry Center, in the release. “This acceleration of digital learning spurred an even greater investment in the tech category. The increase in tech spending, combined with stimulus checks, child tax credits and improving consumer sentiment, are providing additional opportunities for retailers this year as consumers have the confidence to up their spend and shop earlier. Those that can capitalize on the impacts the pandemic has had on consumers—how, what and when they purchase—should be well positioned.”

Digital preferences accelerate online shopping

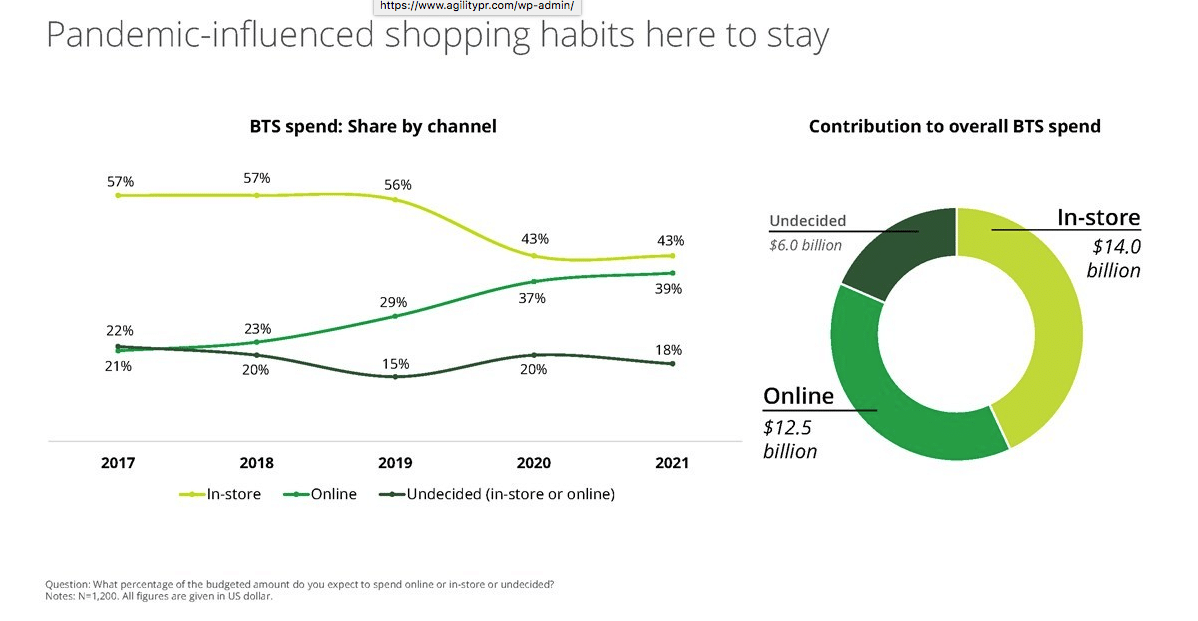

Technology isn’t just impacting what parents buy for back-to-school, it’s driving how they complete their transactions. The level of online spend for back-to-school remains high (39 percent compared to 37 percent in 2020), while in-store spending is flat at 43 percent, demonstrating a fundamental shift in consumer shopping patterns.

- K-12 families plan to spend $12.5 billion online this back-to-school season, up from $10.4 billion last year.

- A majority of consumers plan to use personal computers (67 percent) or smartphones (58 percent) to shop, up from 64 percent and 46 percent in 2020, respectively.

- Additionally, the survey notes that social media is an integral part of the shopping journey for 41 percent of K-12 parents, up 25 percent from 2020. Among those using social media, 42 percent are visiting retailers’ social media pages not only to assess their products, but to get a sense of their personality and purpose, compared to 30% in 2020.

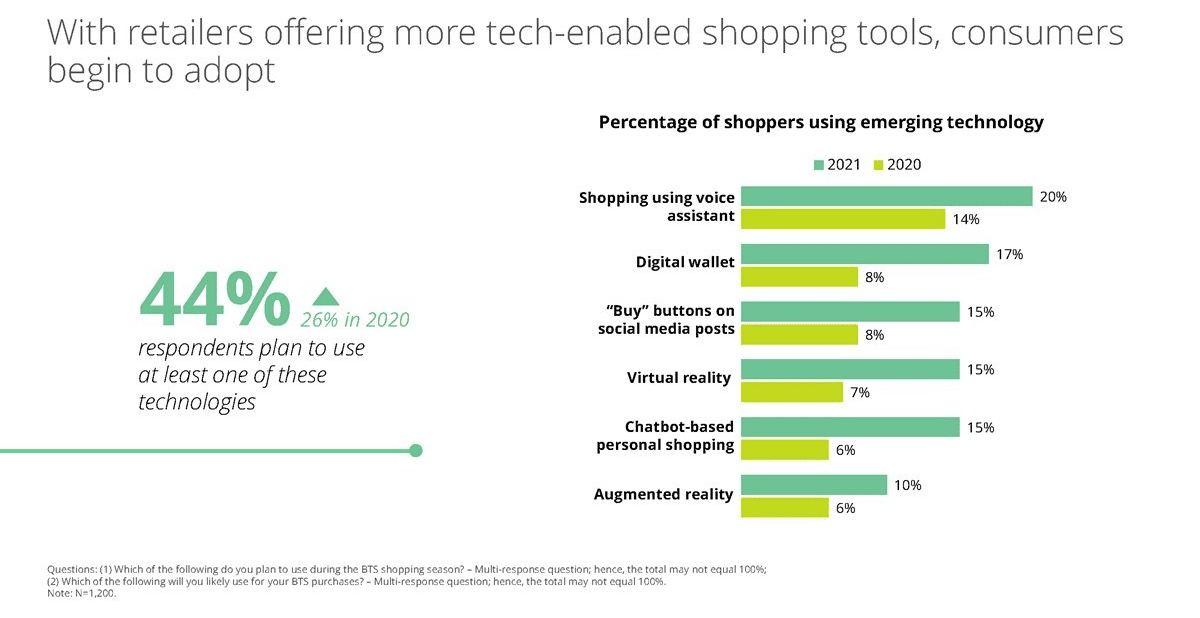

- Further, 44 percent of consumers plan to leverage tech-enabled shopping tools offered by retailers for their back-to-school purchases. Shopping using a voice assistant is the most preferred offering (20 percent) followed by digital wallets (17 percent); and “buy” buttons on social media, virtual reality and chatbots (each at 15 percent).

COVID-19 continues to influence shopping behaviors

Despite consumer optimism and better clarity about the upcoming school year, pandemic-influenced shopping habits are affecting timing and preferences for the back-to-school season. And while online spending continues at high levels, 18 percent of K-12 households remain undecided about where they will do their shopping—representing a $6 billion opportunity for retailers.

- After a year of supply chain challenges, 50 percent of shoppers are concerned about stockouts, especially for tech items. Consumers plan to shop earlier as a result; 59 percent of back-to-school spending will occur by the end of July (versus 45 percent in 2020).

- Although mass merchants remain the most popular retail format to visit (74 percent), online-only stores are the preferred format for tech purchases. Overall, more people expect to shop at online retailers (49 percent) and closer to home at dollar stores (41 percent) compared to last year.

- Fast-fashion and thrift store visits are also on the rise as interest in athleisure (61 percent) and fashionable clothing (57 percent) elevated among higher-income households.

- When selecting where to shop, K-12 parents continue to seek a good deal for their purchases (51 percent), but they also expect improved product quality (48 percent versus 43 percent in 2020).

- Consumers expect the conveniences they adopted during the pandemic to remain available; 34 percent plan to use BOPIS or curbside pickup more frequently for back-to-school shopping.

- Further underscoring the need for convenience, the popularity of preconfigured kits is on the rise with 4 in 10 planning to purchase from PTAs or charities, doubling since the pandemic and providing an opportunity to support their local communities.

Back-to-college spending driven by confidence in the return to campus

As most colleges plan to fully reopen this fall, parents are less anxious about the return to campus (34 percent versus 62 percent in 2020), and more than three-quarters of parents (78 percent) expect their college-age children to be vaccinated by September 2021. Back-to-college parents plan to spend $26.7 billion, or approximately $1,459 per student, up 5 percent from last year.

- The pandemic spurred digital integration for higher education, with expected tech category growth of 17 percent. Meanwhile, spending on traditional college supplies is down 9 percent to $6.8 billion.

- More than one-third (34 percent) of college families expect to spend more on college-items this year. Middle-income families’ spending is set to rebound and surpass pre-pandemic levels. Further, their estimated spend is more than that of higher-income families in computer hardware, while dorm and apartment furniture and electronic gadgets are also seeing renewed investments.

- Pandemic shopping trends linger for college families as well, as they plan to spend $9.4 billion online this fall.

- Despite the preference for online shopping for back-to-college purchases, the overall use of tech shopping tools like digital wallets and voice assistants is lower for back-to-college shoppers (30%) than for back-to-school consumers (44 percent).

- Similarly, the back-to-college consumer is half as likely to use social media to assist in their shopping than those purchasing items for back-to-school (22 percent versus 41 percent).

The “2021 Deloitte Back-to School Survey” was conducted online using an independent research panel between May 27 to June 5, 2021 and surveyed 1,200 parents who have at least one child attending school in grades K-12 this fall.

The “2021 Deloitte Back-to-College Survey” was conducted online using an independent research panel between May 28 to June 17, 2021. The survey polled a sample of 961 parents of children heading to colleges and universities this fall.