New York, July 22, 2025 – The top North American PR Agencies managed to increase revenues, and almost half remained profitable, despite changing marketing forces pushing back against both growth and profitability. The Gould + Partners report was based on the annual survey conducted by the firm for almost thirty years.

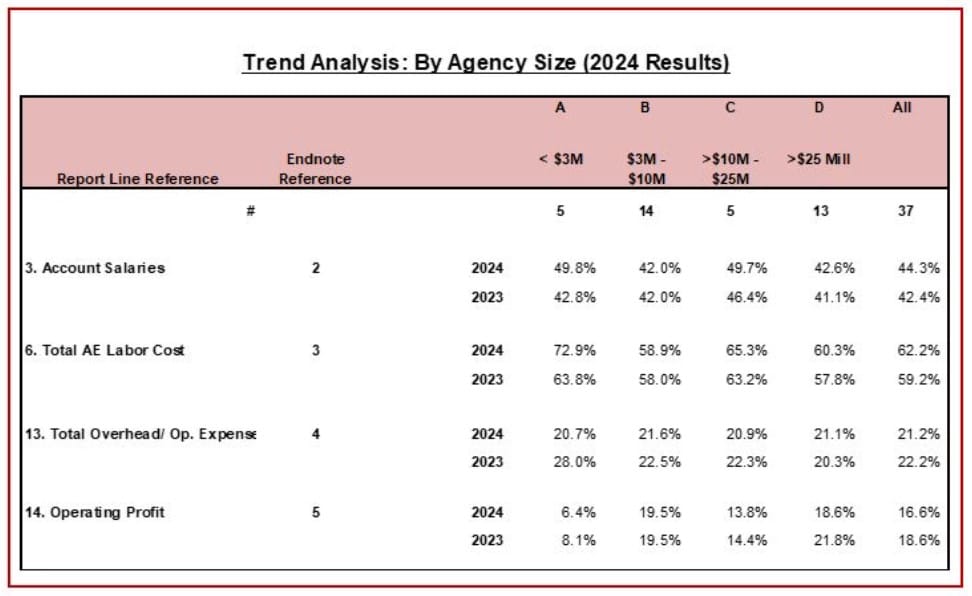

The G+P report that tracked participating firms across 21 critical financial benchmarks found that North American PR agencies generated average Operating Profit of 16.6%, the key metric for firm valuation. This was down 2.0% from 2023. This is the lowest average profitability since COVID 2019’s 17.4%. The decrease was a result of total labor cost increasing from 59.2% to 62.7%. Total labor cost included base W-2 cost (44.3%) plus bonuses, freelance labor, payroll taxes and payroll-related benefits.

The Largest PR agencies- those over $25 Million annually- accounted for operating profit of 18.6% while firms under $3 Million in net revenues were at a weak 6.4%. Firms between $3 Million and $10 Million were at 19.5% and those in excess of $10 Million to $25 Million wera at 13.8%. Budget cuts and consolidation were the main reasons provided by the firms with major drops in profitability. Operating expenses/overhead averaged 21.2%, down from 22.2%in 2023.

The drop in operating profit was also directly attributed to a drop in revenues for many firms. Revenue growth was flat in every category, showing a combined decrease in growth of 1.0%. The Over $25 Million group decreased 1.1% versus an increase a year ago of 2.6%. The over $10 Million- $25 Million were at 3.3% growth, exactly the same as 2023. The less than $3 Million group were a negative 16.6%, further explaining their 6.4% in operating profit.

Revenues per total staff averaged $232,294, down from $240,948 last year. Revenues per professional (subtracting out non-billable administrative staff) was at $264,404, down from $272,672 in the prior year.

The survey also found that in the 10 regions included, the most profitable were D.C. (20.4% and the Midwest (21.3%). The other eight regions ranged from 12.4% (Southwest) to 18.0% (Canadian firms).

For the full report go to Gould+Partners website www.gould-partners.com and click on the link to the report.